How CHC Works

CHC works alongside your insurance—not instead of it.

You still get coverage through a broker.

What’s different is how your premium dollars flow—and how risk is managed over time.

A different way to manage risk — and cost

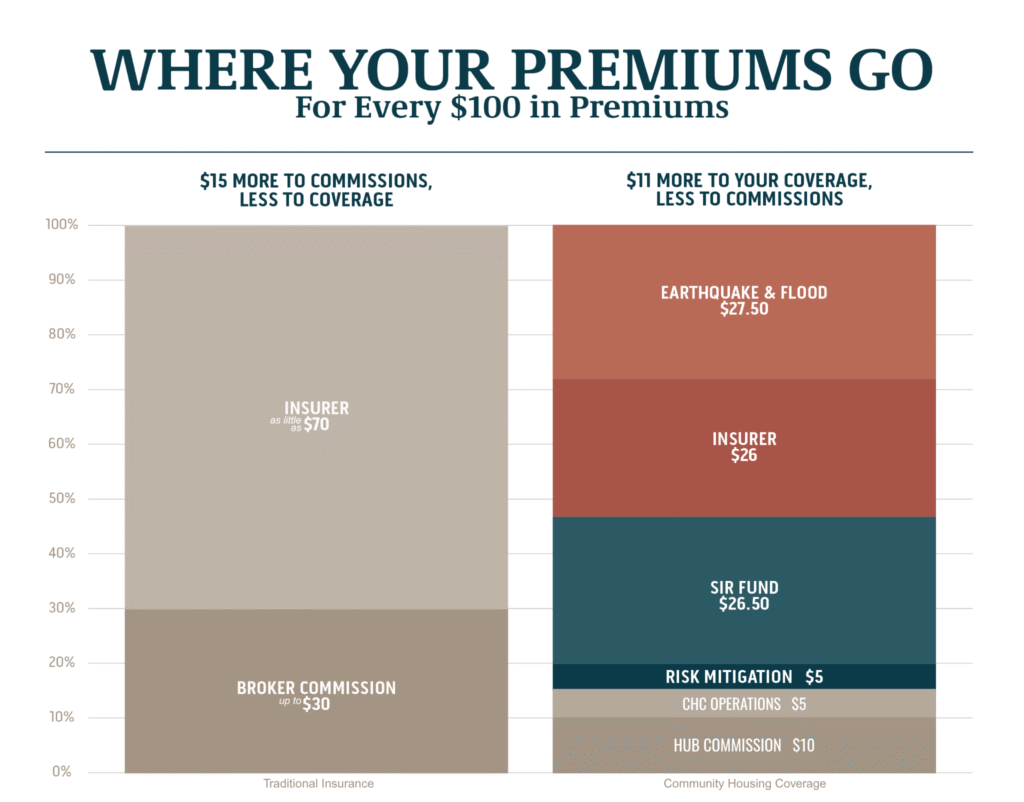

The traditional model:

- Your premium goes to insurers

- Claims go directly to insurers

- Premiums increase after claims

With CHC:

- Members work together

- A portion of your premiums, which you pay anyway, contribute to a shared fund

- That fund helps absorb claims from the deductible up to $250K, before your insurance kicks in

How it works: step by step

You pay your insurance premium

You pay your insurance premium

Just like you normally would

A portion of your premium, which you pay anyway, is set aside in a shared fund

A portion of your premium, which you pay anyway, is set aside in a shared fund

This is the Self-Insurance Retention (SIR) Fund

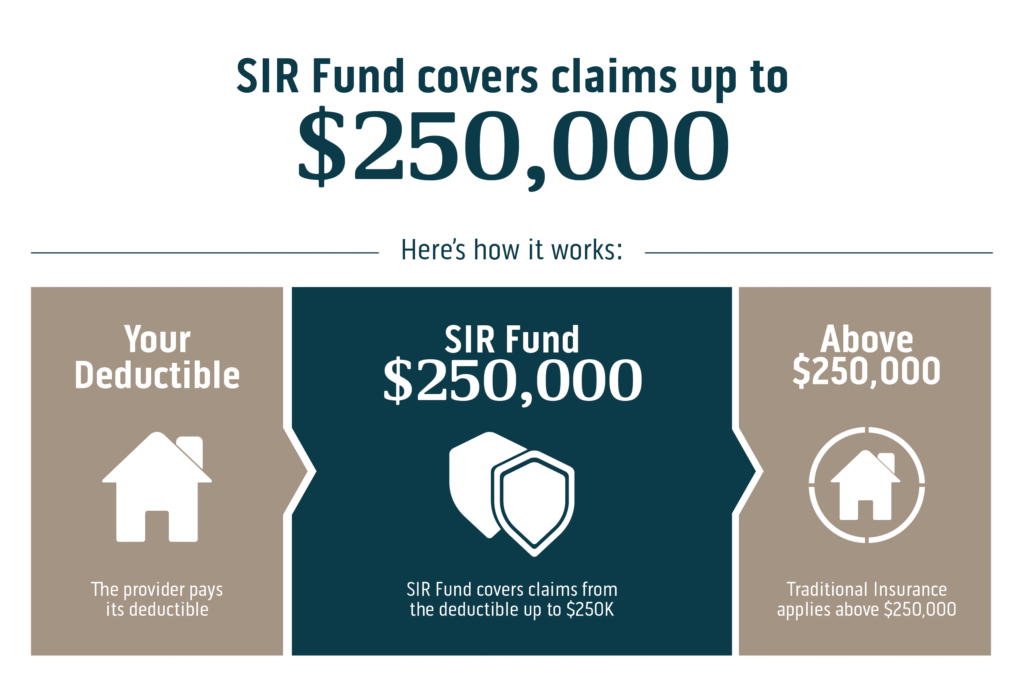

If there’s a claim:

If there’s a claim:

- You pay your deductible

- The SIR Fund covers the next portion

- Insurance only steps in after that

What is the SIR Fund?

The SIR Fund is a shared fund supported through member participation.

It acts like a second deductible, helping cover claims before insurance is involved.

It reduces the number of claims that impact your policy and future pricing.

Because fewer claims go to insurers:

● You’re less likely to see sudden premium increases

● More control stays within the sector

● Your costs start working for you—not just the insurer

Important to know

Being insured through a broker is not the same as being part of CHC.

To access the SIR Fund and its benefits, you must be enrolled in the CHC program—not just hold a standard policy.